You’re interested in claiming research and development (R&D) tax relief to help your business secure funding without diluting the shareholders.

Or you already claim R&D tax relief and wonder if you are overpaying.

There are many R&D firms available in the UK. They charge different fees, provide slightly different services and use various pricing methods.

This guide will help you understand the various ways R&D advisors charge their fees, how much they charge and what makes the prices go up and down.

In the next 12 minutes you’ll learn:

- What the different pricing models really cost

- How the new HMRC changes are pushing fees up for some companies and down for others

- The price tag of an HMRC enquiry

- Simple ways to keep costs low without cutting compliance corners

Fee Structures: Which R&D Pricing Model Works For You?

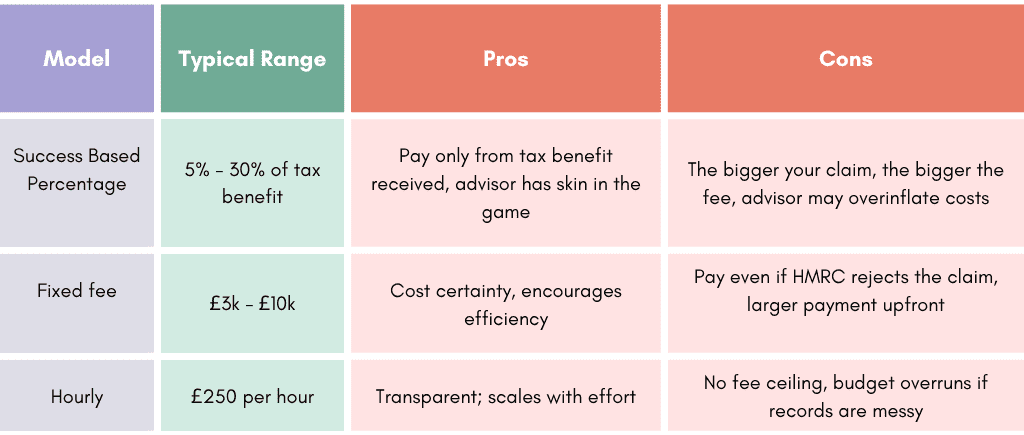

Success Based Percentages

The ‘no win, no fee” structure is very common in the industry. It’s a term that I dislike, so I named it success based percentages.

Under this pricing structure, the fee is charged on the tax benefit as a result of the R&D claim.

The tax benefit includes:

- a reduction in corporation tax

- a refund of corporation tax

- a loss generated and carried forward (or backwards)

- a loss created and surrendered under group relief

- a loss surrendered for R&D tax credits.

There are two types of payment terms.

- Payment is due when the tax benefit is received. The receipt of the tax benefit is usually established by the claimant receiving an R&D payment from HMRC or their online HMRC portal reflecting the changes as a result of the R&D claim.

- As R&D tax consulting has evolved, some firms have decided to base their payment terms on days after submission or completion. For example, R&D Consulting Ltd has payment terms of 28 days from completion of the R&D claim. This method helps these consultancies better manage their cash flow.

The contingent percentage ranges from 30% to 5% of the tax benefit. Contingency fees under 5% rarely cover a senior technical specialist’s time, which is why reputable firms have abandoned “race-to-the-bottom” pricing.

Benefits Of Success Based Percentages

Now let’s cover the pros of using success based percentages.

- Cash Flow Friendly

The claimant only pays once they have received the tax benefit. This maintains better cash flow.

- “Skin In The Game”

The adviser only gets paid once you get paid. There is a perceived lower risk. Additionally, the advisor will try to uncover as much qualifying costs as possible to maximise your benefit and their fee.

Please note, this does not mean that the R&D claim has been approved by HMRC. HMRC can, in most cases, open an enquiry into an R&D claim after two years of submission.

- Built-In Price Cap

If your tax benefit is modest (£2k - 30k), a 15 % fee can be cheaper than a fixed minimum that many specialists charge.

- Flexible Budgeting

Finance teams can treat the fee as a direct % cost of the credit, simplifying ROI modelling.

Downsides Of Success Based Percentages

- Expensive Large Claims

For firms that are scaling, they spend more money on R&D year on year and as a result of this, the fees increase.

A firm that receives an R&D tax credit of £250,000 at a rate of 15% will have a fee of £37,500 plus VAT. A fixed fee may be less.

- Incentive To Push The Envelope

It’s no secret that R&D tax relief has a tainted reputation due to dirty players in the industry. These firms may be tempted to inflate R&D costs, increasing their fees.

- Difficult To Compare Other Success Based Quotes

An R&D tax adviser quoting 20% compared to another quoting 15% sounds clear, until you learn what each advisor includes in their services. You should watch out for:

- Is enquiry defence included?

- Does the contract have multi-year tie-ins?

- Will you be charged a fee even if you do not submit an R&D claim in the following year?

Always read the terms and conditions.

- Multi-Year Lock Ins

Some contracts have a multi - year lock in. You have to remain vigilant, as some of these multi-year lock-ins, charge fees in years that you do not submit an R&D claim, even when you do not have qualifying projects.

- Possible HMRC Wariness

HMRC has publicly flagged “contingent-fee boutiques” as a risk hotspot, which can mean stricter scrutiny. This is especially true when it comes to firms that work on a volume approach and have submitted undefendable R&D claims.

Fixed Fees

The fixed fee model is used mainly by non-specialists like accounting firms that provide bread and butter services such as bookkeeping, tax returns and accounts. They add on services such as R&D tax relief.

There are, however, a few fixed-fee R&D specialists. Additionally, firms that offer success based percentages may occasionally work on a fixed fee basis due to the client's negotiating skills.

Fixed fees can vary from £3,000 up to £10,000. They can be a mixture of payment up front, payment at submission and payment on result.

Benefits Of Fixed Fees

- Total Cost Certainty

As the price is agreed up front, the claimant’s finance team can budget and forecast return on investment with no surprises.

- Better Value On Larger Claims

Fixed fees can result in more benefit for the claimant. As the tax benefit increases, the fee remains the same.

- Less Temptation To Overinflate

As revenue is not aligned with the claim size, there is no financial incentive for the R&D advisor to overinflate claims.

Downsides Of Fixed Fees

- Pay Even If HMRC Adjusts The Claim

If HMRC opens an enquiry and the claim is reduced or rejected, then the claimant will have a lower return on investment as a percentage. If the whole claim is rejected, the client will incur a loss.

- Larger Up Front Cash Hit

Firms charge on submission, so the claimant will have to fund the fee before seeing a tax benefit from HMRC.

- No Incentive To Find All Costs

As the fee is not aligned with the size of the claim, the advisor is not incentivised to identify additional costs.

- Risk of ‘Tight” Scopes

To protect margins, advisors cap meetings and additional charges may be incurred.

- Steep Fees for Smaller Claims

For smaller claims, a fixed fee may be more expensive than a success based percentage.

- Less Obvious Incentive Markers

As advisors get paid regardless of success, you need other trust markers to judge quality, such as employee qualifications, enquiry rates and references.

Hourly Rates

The fee structure for typical accountants and independent R&D consultants is the hourly rate. These rates can vary depending on firm size, location, experience and qualifications.

I have seen hourly rates starting from £250 per hour. Firms with less expertise can charge from £60 per hour.

Benefits Of Hourly Rates

- Pay For Work Done

The fees are tracked by the consultant, so a straightforward claim can cost less than other fee types.

- Full Cost Transparency

Each invoice can be broken into who worked on the project, their rate and the number of hours worked.

- No Incentive To Overinflate Or Underinflate

As the fees are not aligned with the claim size or the success, there is less temptation to add costs to boost the claim.

Downsides Of Hourly Rates

- Budget Creep

With no incentive to complete the R&D claim efficiently, the advisor may have a long process, such as multiple interviews and long meetings.

- Larger Up Front Cash Hit

Many firms charge on submission, so the claimant must fund the fee before receiving a tax benefit from HMRC.

- No Incentive To Find All Costs

As the fee is not aligned with the size of the claim, the advisor is not incentivised to identify additional costs.

- Alignment Gap

The advisor gets paid irrespective of the success of the claim. An enquiry would be very expensive as these can last for months (some have lasted years) and you may need an expert to help defend you. Fees for this start around £250/hour.

- Less Obvious Incentive Markers

As advisors get paid regardless of success, you need other trust markers to judge quality, such as employee qualifications, enquiry rates and references.

What Affects The Costs Of An R&D Tax Claim

Various factors can drive the costs up and down for a service. Below you’ll find the 10 cost drivers that can affect an R&D advisory fee.

1. Size & Shape Of The Claim

A single £500k software project is quicker to document than seven £71k projects scattered across departments. The more qualifying R&D projects a company has, the more technical write-up the advisor has to complete. Each project requires a technical narrative.

Similarly, the greater the qualifying spend, the greater the HMRC scrutiny. The advisor, therefore, has to gather more evidence for HMRC and write a more detailed technical narrative.

The type of R&D scheme affects the claim. If a project spans a time when rules change, such as the introduction of the merged scheme, more work is required by the technical consultants.

2. Technical Complexity

The more complex the R&D claim, the more time it takes for the advisor to understand the project, unravel the costs and write these so HMRC can easily understand it.

The complexity of the project could be aligned with the technical R&D or the tax rules.

3. Evidence Quality & Record-Keeping

Clean accounting records can result in a quicker and easier turnaround for R&D consultants.

Modern accounting software, coupled with good records management, enables R&D firms quicker and easier access to records, saving time.

Additionally, access to Jira, GitHub, lab notebooks and test logs lets the adviser pull proof without pestering your engineers and scientists.

4. Business Structure & History

Complex group and ownership structures add to the workload for R&D consultants. The R&D rules are different for SMEs. Although there has been some alignment between SMEs and larger firms with the introduction of the Merged Scheme, it is still important to establish the SME status of a claimant when it comes to surrendering losses for payable R&D tax credits.

When R&D is undertaken by a subcontracted connected company, the claimant and the subcontractor both require an analysis to establish the amount of costs they can claim. This adds more complexity and workload to the advisor.

A claimant who has failed to defend against an HMRC enquiry is a riskier client. There is a risk that HMRC will open a new enquiry into the new R&D claim. As HMRC R&D Enquiries can take months to defend, it demands a lot of commitment from the advisor.

There could be a premium paid for these claims.

5. Current HMRC Climate

Since 2020, HMRC has increased its R&D compliance team by about 500%, from roughly 100 officers to “over 500 people working on R&D compliance” (GOV.UK) and it now opens compliance checks on about one in five claims (17 % of 2023-24 claims according to HMRC’s statistics, while the HMRC CEO told Parliament the figure is “over 20%”.

As compliance checks are more common, these costs must be absorbed by R&D firms. If HMRC opens an Enquiry into an R&D claim, the work undertaken for that client will lead to a financial loss. If the claim is rejected, the loss will be greater.

In addition, HMRC now requires more information to be provided for R&D claims. This includes the submission of an R&D Claim Notification and the Additional Information Form (AIF).

6. Employee Quality

R&D tax relief is complex. If you require VAT advice, you get a VAT expert. If you require M&A tax consulting, you get an M&A tax expert.

R&D tax is slightly different. You require someone who understands the tax elements and another person who understands the technical R&D elements.

This means that R&D firms have both tax specialists and sector experts to enable them to identify more qualifying opportunities for clients.

Tax specialists are in high demand, especially in R&D tax relief. An experienced R&D consultant with a tax qualification (ATT or CTA) are even rarer and with this expertise, they command a high salary.

Sector experts such as Chartered Scientists, PhDs and software engineers command higher salaries to move from their already well-paid sector.

As these employees are in high demand from competitors, they receive great benefit packages.

London-based staff with higher salaries bump up costs. Covid has now altered this slightly with home working.

7. Referral Fees To Accountants Or Introducers

Many firms that provide R&D tax services share 10% - 30% of the R&D fee with the referring accountant or introducer.

8. Delivery Method

The methodologies used to prepare the R&D reports are packaged differently.

- DIY methods charge less, but the workload shifts towards your team. This delivery method is popular with R&D software services and with generalist accountants who add the claim to year-end work.

- A specialist consultancy handles most of the heavy lifting and, in most cases, provide an end to end service.

9. Location

Firms that have offices in areas where premises are expensive, especially in London, have greater office costs.

How To Spot Hidden Charges In An R&D Contract

There are many activities when it comes to delivering R&D consulting, from preparing the financials, writing the technical report, to completing the two online forms (AIF and R&D Notification).

Hidden fees can relate to HMRC Enquiry services, up front charges, payment terms, exit fees, multi-year lock ins and the list can go on.

Here are the 5 terms and conditions that you should look out for.

- Scope creep clauses - Do extra meetings, submission of the Additional Information Form or revision of tax computations trigger extra billing?

- Enquiry defence coverage - Is support included for HMRC Enquiries or do they incur additional costs?

- Exit fees (I hate this one) - Some contracts lock you in for future years and if you don’t submit an R&D claim using the advisor, it triggers a fee.

- Payment triggers - Firms charge for “invoice on submission” and “invoice on HMRC payment.” An invoice on submission means that the advisor wants payment when the R&D claim is submitted to HMRC or within X days of submission. An “invoice on HMRC payment” relates to when the client sees the tax benefit (explained above).

- Minimum fees - Smaller claims have less profit margin, so firms have introduced minimum fees. I have seen these ranging from £1,500 to £3,000.

Practical Ways To Reduce R&D Claim Costs Without Risking Compliance

You can use these improvements to help negotiate lower fees.

- Nail The Records - Use project codes for every R&D task. This makes it quicker and easier for you and the advisor to identify qualifying R&D costs.

- Multi-Year Commitment - Lock in a 3 year contract and negotiate the fee curve up-front. Advisers discount when future work is guaranteed.

- Leverage Advance Assurance - For first-time SMEs, HMRC pre-approval can cut enquiry risk and therefore advisory premiums.

- Pre-Agree Enquiry Work Fees - Negotiate a capped-hour bank or include defence within the core fee, as surprises during an HMRC enquiry are always expensive. This is for fixed fee or hourly fee structures.

- Nominate Internal R&D Champion - One point of contact keeps questions moving and avoids the “reply-all delay” that racks up hourly charges.

- Opt for digital collaboration - Grant read-only access to your accounting, payroll and Git/Jira systems.

- Standardise Evidence Capture - Create a one-page “R&D snapshot” template (objectives, uncertainty, breakthroughs, team involved) and have project leads fill it in monthly.

What an HMRC enquiry can cost you

As this is currently a hot topic, I have included information about the costs of an HMRC R&D Enquiry.

An HMRC R&D enquiry is a resource drainer as it can take many months to clear. It involves a lot of back and forth with HMRC, usually by letters. In most cases, after 3 replies HMRC is open to a meeting (face to face or online) to discuss the R&D claim.

It is important to know how your R&D advisor charges you for any HMRC Enquiries. Most firms that charge a success based percentage tend to include enquiry defence in their contracts, but you should still look for this confirmation in the contract.

The firms that deliver R&D services on a fixed fee or hourly fee basis usually have extra charges for HMRC enquiries.

The information is limited on how much firms charge for enquiry work; again, it works on various fee models.

I have seen specialist defence fees ranging between £250 and £350 per hour.

As an estimate, the back and forth with HMRC, plus a face to face meeting, will cost £7,000 plus VAT. This is based on 20 hours of work.

You’re Now Prepared To Speak To A Firm About R&D Tax

You now know:

- The three pricing models and what they really cost.

- How HMRC’s 2025 crackdown is reshaping adviser fees.

- What affects the costs of R&D advisors.

- Practical moves to cut fees without cutting corners.

- Why an enquiry can cost more than the original claim if you’re not prepared.